“`html

Key Takeaways

- Business Development Companies (BDCs) offer high dividend yields, potentially exceeding 12.9%, making them attractive for income investors.

- However, BDCs carry risks, particularly those overly specialized in a single sector or burdened by high management fees, which can erode shareholder returns.

- Examples like TriplePoint Venture Growth BDC Corp. (TPVG) and Goldman Sachs BDC (GSBD) illustrate these risks, showing underperformance relative to benchmarks and potential dividend cuts or insufficient coverage due to fees and portfolio losses.

- Closed-End Funds (CEFs) investing in blue-chip stocks are presented as a safer alternative, offering competitive yields and total returns with greater stability.

- The Columbia Seligman Premium Technology Growth Fund (STK) is highlighted as an example of a CEF with a strong track record, consistent dividends, and a discount to its Net Asset Value.

Understanding Business Development Companies (BDCs)

Business Development Companies (BDCs) have been gaining traction, yet they often fly under the radar for many investors. This is a missed opportunity, as BDCs can deliver substantial dividend income, with some offering yields exceeding 12.9% annually.

For retirees or those seeking to augment their portfolio income, a $10,000 investment in such a BDC could generate over $1,290 in annual dividends. These entities also play a crucial role in supporting middle market companies—businesses too large for local banks but too small for major institutional investors like Goldman Sachs.

While BDCs are becoming more recognized, it’s crucial to approach them with caution, especially in the current market environment. Recognizing and avoiding specific pitfalls is key to successful BDC investing.

Navigating BDC Risks: Specialization and Fees

Two primary risks can significantly impact a BDC’s performance: excessive specialization in a single industry sector and burdensome management fees.

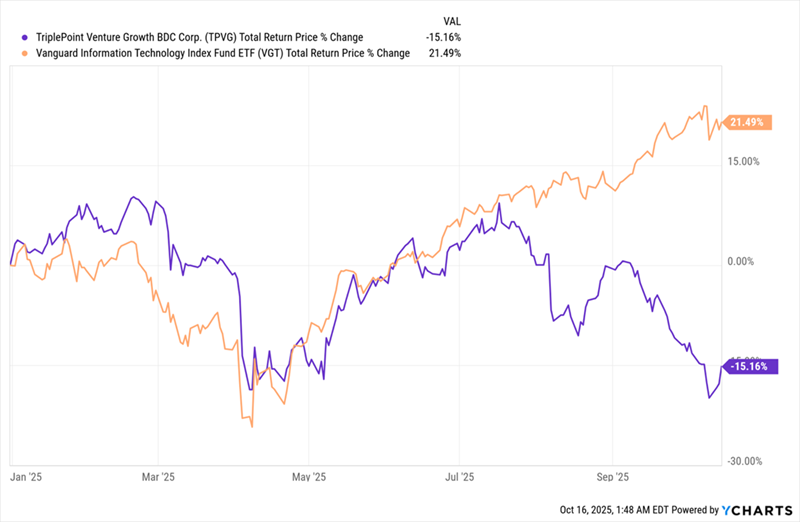

Sector Specialization: The TriplePoint Venture Growth BDC Corp. (TPVG) Example

Consider TriplePoint Venture Growth BDC Corp. (TPVG), which boasts a remarkable 16.6% yield. This BDC primarily focuses its lending activities on technology companies. However, despite its high dividend, TPVG has experienced a 15% decline in total return this year, including reinvested dividends. This performance is notable, especially when contrasted with the broader tech sector, which, as measured by the Vanguard Information Technology ETF (VGT), has seen gains of over 21%.

This situation highlights that even a high dividend yield cannot compensate for fundamental underperformance, and in some cases, diversified investments like ETFs or specialized closed-end funds (CEFs) focused on the same sector might offer superior total returns.

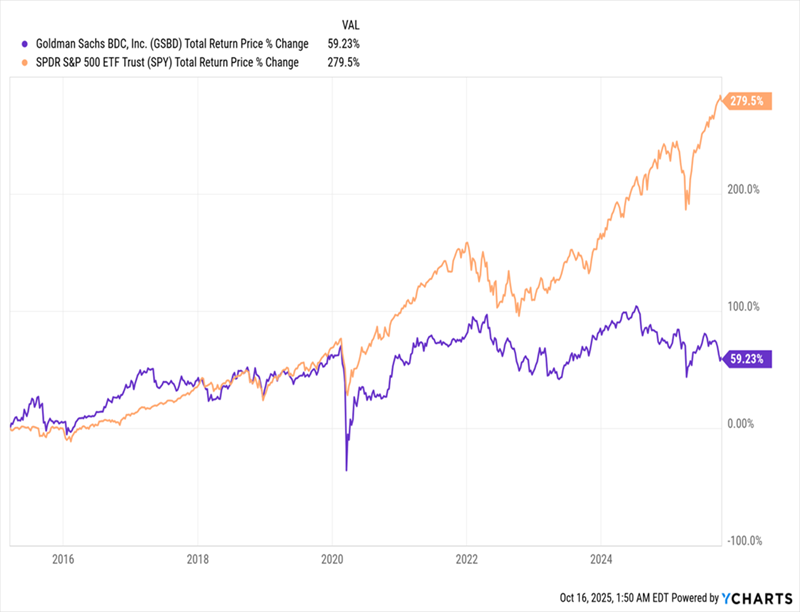

High Management Fees: The Goldman Sachs BDC (GSBD) Case

Another significant challenge for BDCs is high management fees, which can easily be overlooked by investors focused solely on yield. Many large financial institutions, including Goldman Sachs, have launched their own BDCs to participate in this market.

Goldman Sachs BDC (GSBD), yielding 12.9%, has shown a considerable lag in performance compared to the S&P 500 since its inception a decade ago.

In 2024, GSBD incurred approximately 3.9% in fees—consisting of $35.2 million in base fees and $23.9 million in incentive fees on roughly $1.5 billion in assets. A similar fee burden is expected for 2025. Such high fees can strain a BDC’s ability to generate sufficient profits to sustain its dividend payouts.

Investors are often drawn to GSBD’s attractive yield without scrutinizing the impact of these substantial fees on its actual profitability and dividend sustainability.

Analyzing Dividend Sustainability and Portfolio Health

While the primary appeal of BDCs for income investors is their high dividend payouts, the reliability of these dividends can vary. BDCs aim to generate income from larger deals that cover operational costs and provide dividends. However, this strategy isn’t always successful.

Both GSBD and TPVG have faced challenges in maintaining their dividend payouts. TPVG notably cut its regular dividend last year, resulting in reduced income for shareholders. Consequently, its 16.6% yield, while high now, may shrink in the future, potentially leading to further share price depreciation.

GSBD’s dividend history might appear more stable, with payouts increasing since its IPO. However, a closer look at its income statement reveals underlying issues.

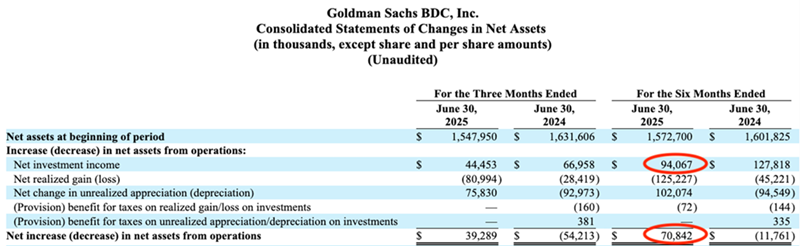

In the first half of 2025, GSBD reported $94.1 million in investment income, translating to an annualized return of approximately 12.4% on its net assets. This rate is slightly below its 12.9% dividend yield, indicating a potential shortfall in dividend coverage.

The situation is further complicated by a $125 million portfolio loss during the same period. After accounting for these losses, the net annualized return from the portfolio’s good loans was 9.4%. While still respectable, this figure is insufficient to fully cover the dividend. If this trend persists, GSBD might face dividend cuts of around $0.40 per share, reducing its yield from 13% to approximately 9%.

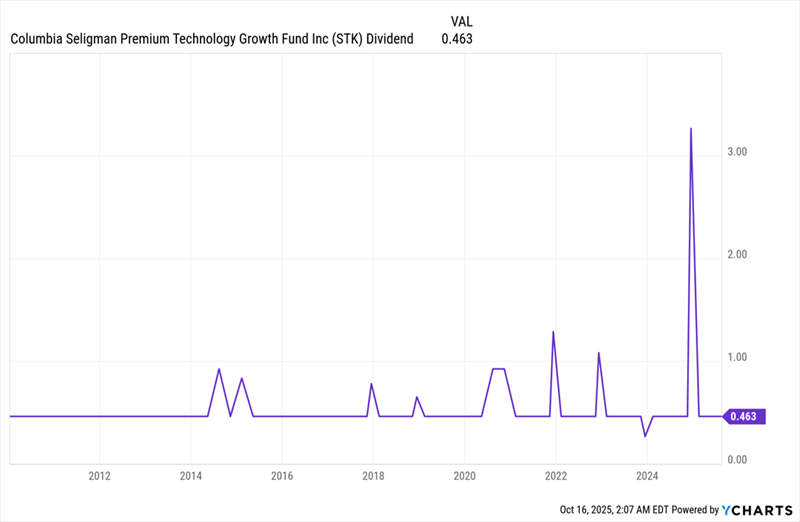

An Alternative: The Columbia Seligman Premium Technology Growth Fund (STK)

Not all BDCs are inherently risky; careful selection based on management, lending practices, and portfolio diversification is essential. BDCs can be exposed to risks like the bankruptcy of companies they lend to, as seen with auto parts supplier First Brands, which impacted 14 BDCs (though not GSBD or TPVG).

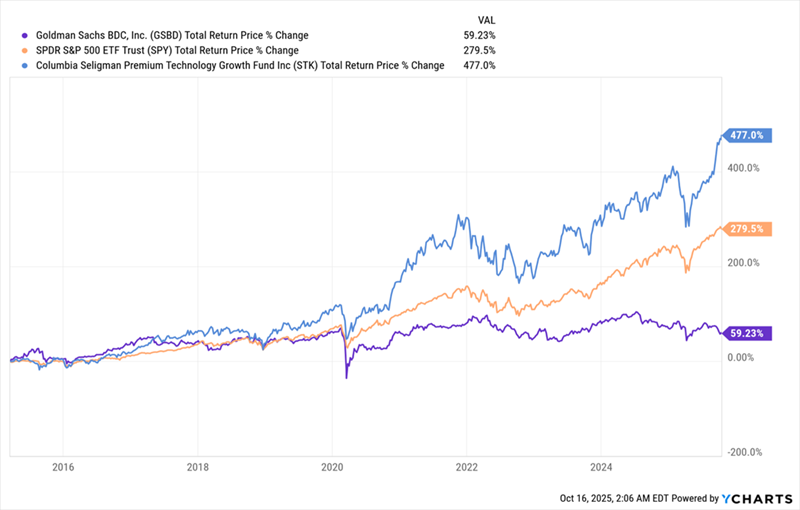

For investors seeking a more stable income stream and capital appreciation, Closed-End Funds (CEFs) that invest in blue-chip stocks offer a compelling alternative. The Columbia Seligman Premium Technology Growth Fund (STK) serves as an excellent example.

Over the past decade, STK has demonstrated impressive performance, outperforming both the S&P 500 and GSBD.

STK offers a 5% dividend yield that has remained consistent and has been supplemented by special dividends over time.

The fund achieves this by investing in established mega-cap technology companies such as Apple (AAPL), Amazon.com (AMZN), and Cisco Systems (CSCO).

Currently, STK is trading at a 5.3% discount to its Net Asset Value (NAV), which is below its five-year average premium of 3.1%. This presents an opportunity to acquire its portfolio of technology stocks at a discount.

STK offers a more secure alternative to sector-specific BDCs. Furthermore, its 5% yield is modest compared to the average CEF yield of 8.4%, suggesting investors can potentially increase their income by diversifying into other higher-yielding CEFs without compromising risk.

Exploring High-Yielding CEFs

The landscape of CEFs offers numerous opportunities for substantial yields, often available at attractive valuations. Even in the current market, compelling income-generating assets can be found.

The top four CEFs recommended for investment currently offer an average yield of 9.5%, providing rich dividends regardless of market conditions.

These funds, holding a mix of bonds and stocks from well-known companies, are trading at discounts, suggesting potential price appreciation of over 20% on average in the coming year, in addition to their significant income payouts.

Final Thoughts

While BDCs can provide high dividend yields, they come with inherent risks related to sector concentration and management fees, as demonstrated by TPVG and GSBD. The Columbia Seligman Premium Technology Growth Fund (STK) serves as a strong indicator of how CEFs investing in quality assets can offer a more stable and potentially more rewarding investment proposition. Investors seeking enhanced income may find further opportunities in other high-yielding CEFs trading at attractive discounts.

“`